Quick answer:

Home Stock Movers MOBX Stock Jumps 82.9% on Tomahawk Missile Defense Contract Win Updated: May 14, 2026 at 11:40 AM ET · Reading time: 4 min · Author expertise: Small-Cap Equity Analyst Why trust us: We separate factual market inputs from interpretation and link our process below. Methodology · Data sources · Editorial policy 💼 Earnings Whisper & Guidance Context 📅 Next Earnings: 2026-08-11 TBD Data: Finnhub.

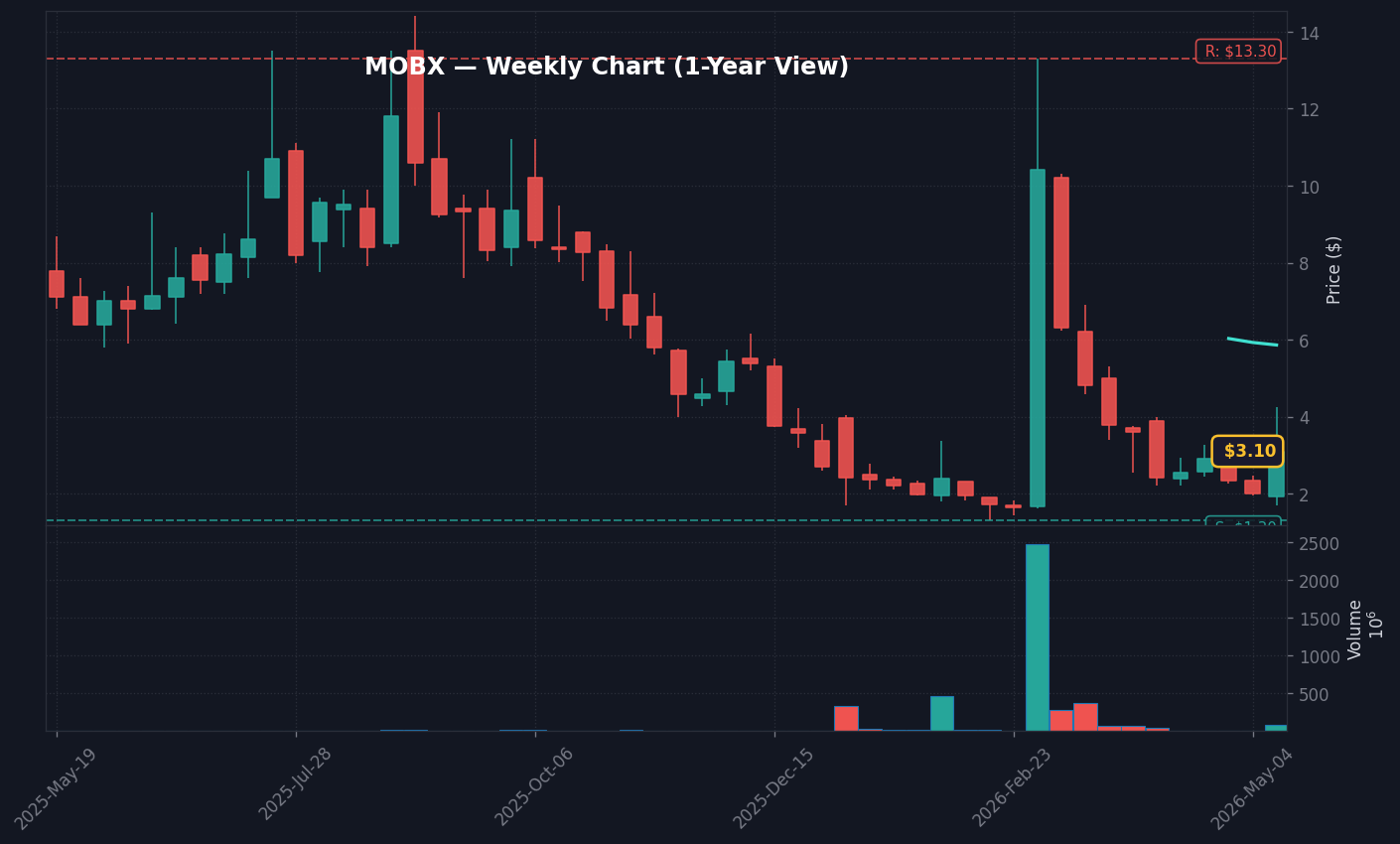

Mobix Labs, Inc. (MOBX) moved +82.9% to $3.18 as traders reacted to a catalyst-driven move. The catalyst still needs follow-through confirmation.

Jungwook Shin, The Stock Radar

The catalyst is everything in short-term equity analysis. Get the catalyst wrong, and nothing else in the analysis matters. Get it right, and you have a framework for the entire move. MOBX surged 82.9%. An M&A announcement is behind the move — either as an acquirer or acquisition target, the deal math is what the market is pricing. Let me take you through what I found in the filings and what it means for the stock.

Heads up — Mobix Labs, Inc. (MOBX) just surged 82.9% on news of a strategic defense contract for Tomahawk missile components.

Mobix Labs, Inc. (MOBX) shares climbed 82.9% today, driven by the announcement of a new defense contract focused on components for the Tomahawk cruise missile system. The market is reacting to the company’s shift toward high-specification aerospace and defense applications, a move that provides much-needed visibility for a firm with a trailing net income of -$10.1M, as noted in its latest filings. Our comfort level with this catalyst is partial, as investors must balance the potential for long-term revenue growth against the historical tendency for thin-float equities to experience extreme volatility after headline-driven spikes.

The macro backdrop remains sticky, with CPI at 3.9% per April 2026 data and the Fed Funds Rate holding at 3.64%. In this environment, markets are penalizing growth-stage companies without immediate profitability unless they land clear, identifiable revenue streams. The move in MOBX represents a pure idiosyncratic event that decoupled from the broader market; while the S&P 500 rose 0.83% and the technology sector (XLK) gained 1.71%, MOBX’s 82.9% surge created an alpha of over 81%, suggesting the market is re-rating the firm based on the defense narrative rather than broader index flows.

What This Company Does

Mobix Labs, Inc. (ticker: MOBX) is an Irvine, California-based semiconductor company that designs and sells advanced wireless and wired connectivity components. According to company filings, the firm specializes in radio frequency (RF) systems, millimeter wave (mmWave) technology, and EMI filtering products. Its customer base spans critical infrastructure sectors, including aerospace, defense, automotive, and medical industries.

Per the latest S-1 filing, Mobix Labs maintains a market cap of $32.68M. The business model centers on delivering high-performance connectivity to complex hardware environments, effectively serving the growing demand for secure, interference-free communications in military and industrial hardware.

Why It Moved Today

The primary driver behind the 82.9% move is the confirmed win of a defense contract specifically for Tomahawk missile components. Headlines surrounding the contract, as reported by outlets like Insider Monkey, caught the attention of retail traders given the company’s small float of roughly 8.3 million shares and high short interest of 15.1%. When news of this caliber hits a low-float, high-short stock, the liquidity constraints often force a rapid repricing as shorts look to cover, which validates the high volume observed during the session.

It is worth noting that while this contract provides a tangible catalyst, the company’s 8-K filings show a revenue base of just $5.7M for the period ending March 2025. This deal represents a potential pivot toward a more stable, government-backed revenue stream, though skeptics should note that the company reported an operating margin of -471% and a current ratio of 0.11, signaling significant liquidity and balance sheet hurdles. I’d lean cautious on the sustainability of the move until the company provides more granular detail on the multi-year value of the contract.