According to Yahoo Finance, Worth a closer look at Ambiq Micro (AMBQ) after today’s 27.0% surge—here is the read on the move and the technicals.

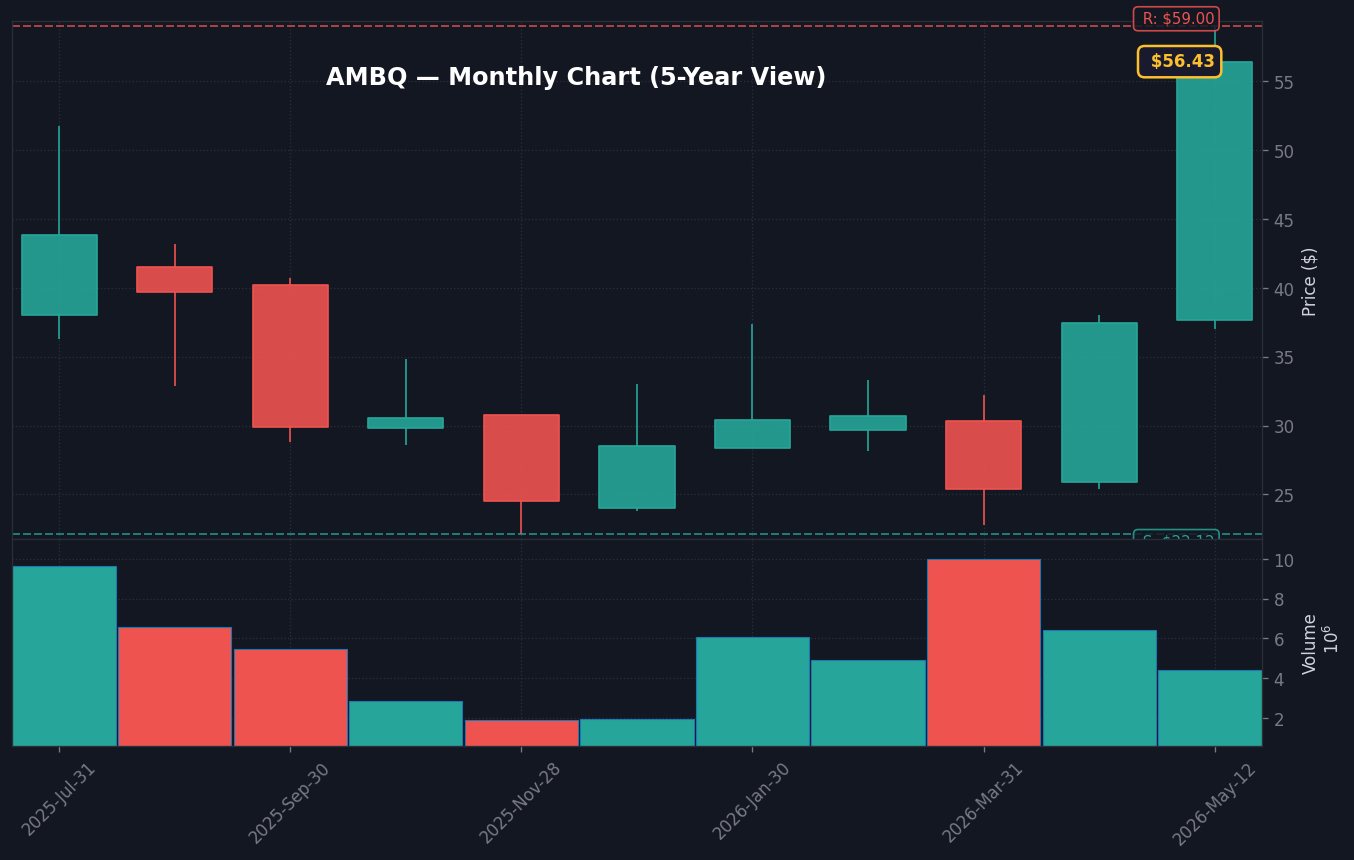

AMBQ shares spiked 27.0% today, driven by the company’s Q1 financial report, which saw revenues top analyst estimates despite a persistent net loss. The move stands out because it occurred during a session where the S&P 500 fell 0.55% and the tech-heavy XLK sector slid 1.42%, confirming the move is purely idiosyncratic and tied to company-specific strength rather than broader market momentum. Our comfort level with this catalyst is partial; while top-line growth is encouraging, the company’s negative operating margins—reported at -57.66%—mean the market is pricing in long-term AI potential over immediate profitability.

Investors should watch how the stock holds above its 20-day VWAP of $39.48, as the current RSI reading of 83.01 indicates overbought territory. What’s driving this is a clear decoupling from the macro environment; with a 1-year beta of 2.8, AMBQ’s alpha today of +28.54% is significant, suggesting institutional accumulation following the earnings print.

What This Company Does

Ambiq Micro, Inc. (AMBQ), headquartered in Austin, Texas, is a semiconductor firm that specializes in ultra-low-power microcontrollers and systems-on-chip (SoC). The company leverages its proprietary Subthreshold Power Optimized Technology (SPOT) platform to reduce power consumption in battery-powered edge AI applications, per Wikipedia. By targeting devices such as smartwatches, fitness trackers, and AR/VR glasses, the firm aims to enable real-time, on-device AI processing without the typical thermal or power constraints of traditional hardware.

Incorporated in 2010 and going public in 2025, the company maintains a unique niche within the semiconductor industry. With a market cap of approximately $1.22B, Ambiq operates in a competitive space, relying on its proprietary AI-acceleration and memory innovations to maintain its competitive moat. The company distributes its products through both a direct sales force and a global network of distributors.

Why It Moved Today

The 27.0% pop is directly tied to the company’s latest financial disclosure. According to the 8-K filed on 2026-05-12, the firm managed to beat revenue expectations despite broader headwinds in the semiconductor space. The story looks solid because the revenue beat implies growing demand for its edge AI solutions, which have historically been a difficult segment to monetize. However, the market seems to be overlooking the net loss of $25.8M as of the September 30, 2025, 10-Q filing, favoring the growth narrative instead.

The real story is the intensity of the buying volume. With 5.87% of the float held short, the move was likely exacerbated by a short squeeze. Per Zacks news, the reaction to these earnings shows that investors are willing to reward tech firms that demonstrate top-line expansion even when operating margins remain negative. This reflects a risk-on sentiment for specific sub-sectors of semiconductors, despite the broader market’s decline.