What happened:

Home Stock Movers PROG Holdings (PRG) Jumps 24.1% on Q1 2026 Earnings Beat Updated: April 29, 2026 at 04:17 PM ET · Reading time: 4 min · Author expertise: Small-Cap Equity Analyst Why trust us: We separate factual market inputs from interpretation and link our process below. Methodology · Data sources · Editorial policy 💼 Earnings Whisper & Guidance Context Quarter Est EPS Actual EPS Surprise 2026-03 $0.80 $1.24 ✓ Beat (+54.4%) 2025-12 $0.60 $0.58 ✗ Miss (-3.3%) 2025-09 $0.75 $0.90 ✓ Beat (+20.5%) 2000-06 $0.11 $0.10 ✗ Miss (-3.7%) 📅 Next Earnings: 2026-07-21 TBD Data: Finnhub.

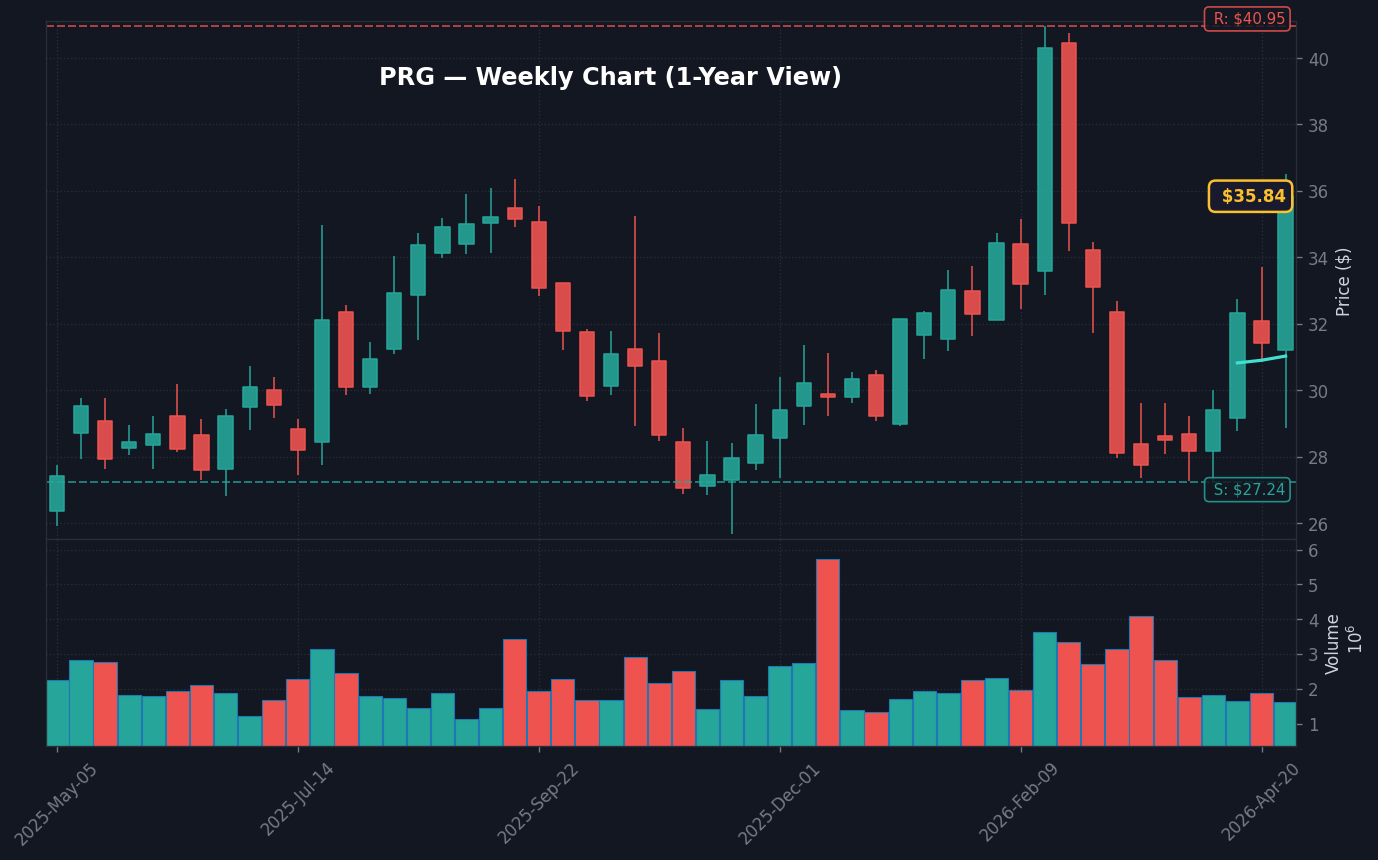

Heads up — PRG just popped 24.1% on the back of a strong Q1 earnings release. Here is the read.

PROG Holdings (PRG) shares vaulted 24.1% today, significantly outperforming broader indices as investors digested a series of quarterly beats. The primary catalyst, per the 10-Q filed 2026-04-29, was a robust earnings performance that topped consensus estimates, shifting the stock’s internal momentum. My comfort level with this catalyst is high, as the move occurred on 2.1x relative volume, suggesting institutional accumulation rather than retail-driven churn.

The real story here is the stock’s decoupling from the broader market. While the S&P 500 slipped 0.04% and the industrials sector (XLI) fell 0.61%, PRG’s 24.12% gain represents a massive idiosyncratic alpha event. This indicates the move is entirely tied to the company’s specific fiscal health rather than a broader sector rotation.

What This Company Does

PROG Holdings, Inc. is a financial technology holding company based in Draper, Utah. The company operates through two primary segments: Progressive Leasing, which provides point-of-sale lease-to-own solutions, and Four, a buy-now-pay-later (BNPL) platform. Per corporate filings, the company focuses on providing flexible payment alternatives for customers with varying credit backgrounds, effectively serving the underserved retail consumer market.

Founded in 1955, the firm manages a complex balance sheet with $2.0B in total assets as of the first quarter of 2026. The firm’s business model depends on consumer spending velocity and the repayment success of its lease-to-own programs, which are currently experiencing a transition in operational focus as detailed in the 10-K filed in February.

Why It Moved Today

The +24.1% surge is driven by an earnings report that Moby noted confirmed a clear beat on estimates. Revenue for the period hit $742.7M, and diluted EPS reached $0.89 per the SEC filings. This earnings performance validates the bullish stance held by the 9 analysts currently rating the stock a Buy, as the company effectively navigated a macro environment characterized by a 4.3% unemployment rate and 3.3% YoY CPI.

Our conviction here is elevated because the volume profile—1.12 million shares traded compared to an average of roughly 535,000—confirms that the move wasn’t just headline noise, but a structural re-pricing. When comparing this to historical analogs, PRG has often seen volatile reactions to earnings, but the 2.1x relative volume sets this specific move apart from previous quarters where the stock struggled to find sustained conviction.