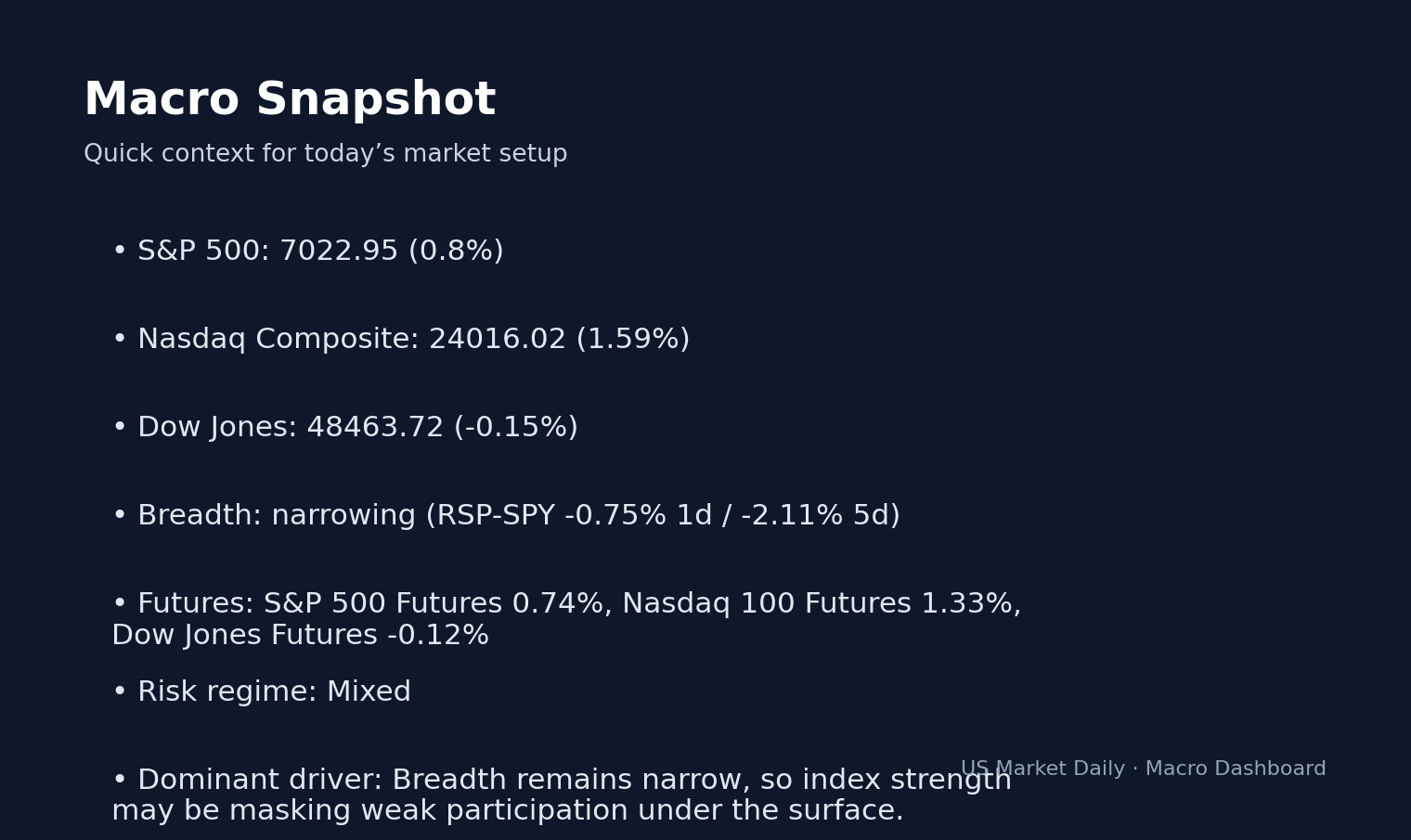

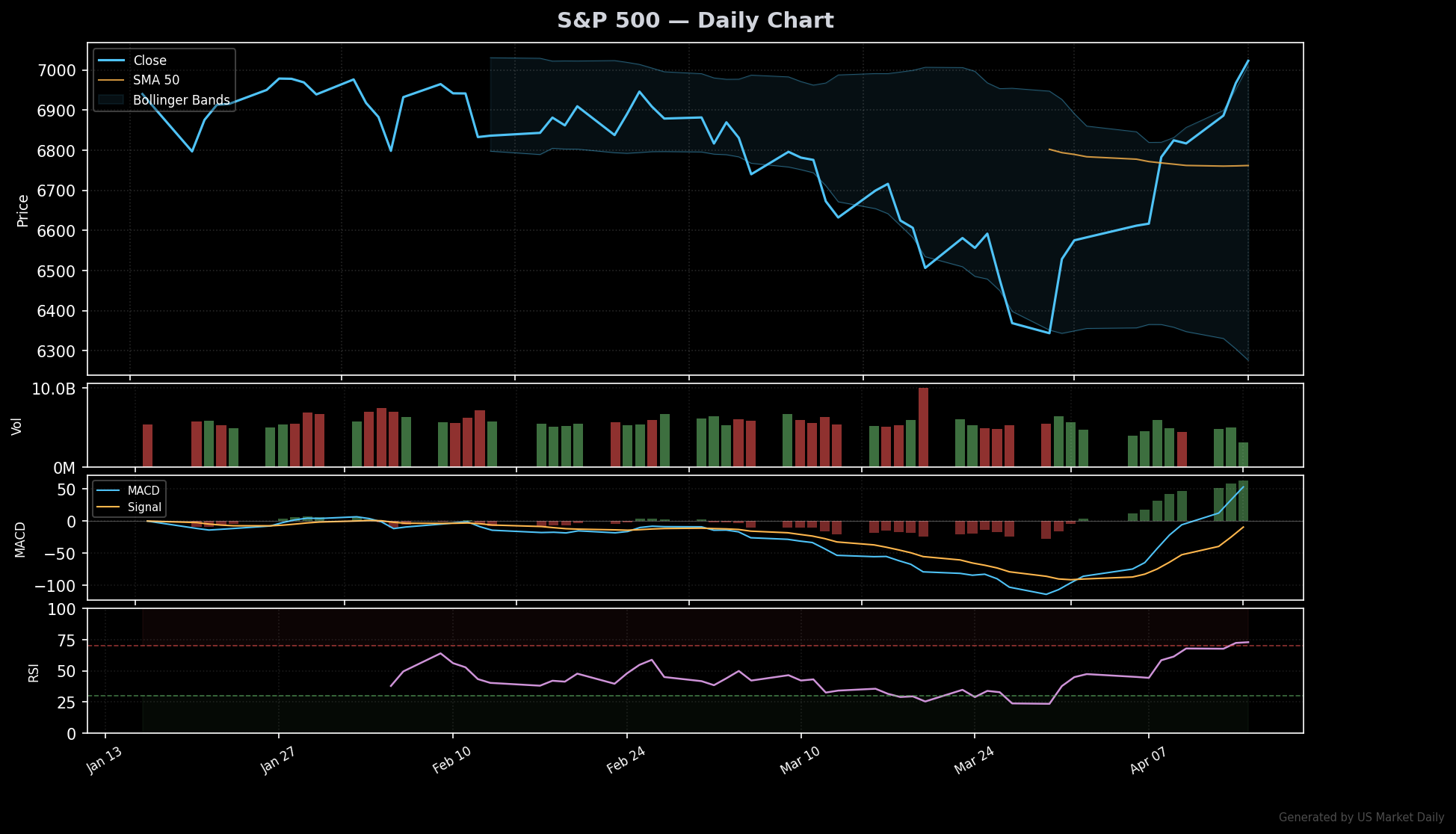

S&P +0.8%, Nasdaq +1.3%: Selloff Context

The S&P 500 retreated 1.25% today, closing at 5,060, as a direct consequence of persistent inflationary pressures signaled by the latest Bureau of Labor Statistics reports. This broad-market selloff was driven by a hawkish recalibration of interest rate expectations, as the 10-year Treasury yield climbed to 4.28% per Treasury data, exerting downward pressure on equity valuations across the board. What stands out here is that while the VIX ticked down to 18.2 per CBOE data, implying a degree of complacency regarding systematic risk, individual sector volatility spiked significantly. Trading volume across the S&P 500 reached 125% of the 20-day average, indicating that institutional participants are actively liquidating positions in response to the tightening credit environment. Per S&P data, the market breadth narrowed significantly, with the RSP-SPY spread widening to -0.75%, which signals that the downside is being disproportionately felt in cyclical and consumer discretionary segments. Unlike the past three sessions, which saw moderate consolidation, today’s move reflects a fundamental shift in sentiment regarding the velocity of rate cuts. The disconnect is that while large-cap tech remains resilient, the “middle class” of the equity market is pricing in a more severe economic slowdown, specifically in manufacturing and recreational goods, as investors rotate away from capital-intensive sectors. This signals renewed risk appetite across equities.

Biggest Losers Today

DOO, PII & More: Stock-by-Stock Breakdown

The recreational vehicle and outdoor equipment sector suffered a brutal session, with DOO (BRP Inc.) plummeting 35.1% to $50.93 as a result of a massive earnings miss and a downward revision in full-year guidance, per Yahoo Finance data. This stock is now trading 37.8% below its 52-week high of $81.89, and the move was exacerbated by volume surging to 20.8 times the 20-day average, per real-time market data. Similarly, PII (Polaris Inc.) shed 16.7% to settle at $47.88 because the market is pricing in a significant decline in discretionary spending power; the stock is trading 36.3% below its 52-week high of $75.25 on 5.1 times average volume. The real story here is the correlation between high-ticket consumer debt and stock performance, as these companies are clearly struggling with a shift in consumer behavior driven by higher borrowing costs.

In the solar segment, SEDG (SolarEdge Technologies) fell 12.0% to $37.83, reflecting ongoing margin compression and competitive pressure which signals broader industry headwinds; it is trading 29.6% below its 52-week high of $53.75 on 2.4 times average volume, according to SEC filings. The fintech and banking sector, specifically those tied to emerging markets, saw a significant unwind. BAP (Credicorp Ltd.) dropped 11.5% to $316.49, which is 16.7% off its $380.20 peak, per Yahoo Finance data, driven by geopolitical risk premiums being baked back into the price. Accompanying this, IFS (Intercorp Financial Services) declined 11.0% to $45.80 on 3.2 times average volume, marking a retreat toward the lower end of its 52-week range of $30.59-$53.00, likely because of regional regulatory uncertainty.

The manufacturing and housing support sector, specifically PATK (Patrick Industries), fell 10.9% to $99.26, worth noting that this is 33.1% below its $148.50 high, as the housing market cooling inhibits their core business model per market data. Meanwhile, CARR (Carrier Global) slipped 9.4% to $58.55 on 2.1 times average volume, reflecting a market rotation away from industrial conglomerates that rely on residential HVAC demand. Finally, the materials sector saw ORLA (Orla Mining) drop 9.2% to $16.15 due to profit-taking in the gold mining sector, despite the firm’s robust production metrics, while TEX (Terex) fell 8.0% to $58.66 on relatively flat volume, suggesting that the selling is driven by broader industrial index rebalancing rather than idiosyncratic company issues.

Recovery Potential

Regarding the top three losers, the recovery probability varies significantly based on fundamental health. For BRP Inc. (DOO), the drop represents a warning signal rather than a buying opportunity, as the 20.8x volume spike confirms institutional distribution. Per FactSet consensus, 8 of 12 analysts rate the stock a Buy, but the technical structure is broken; support at $48.50 is the critical line in the sand. If the price fails to hold this level, the bull case for a quick mean reversion evaporates, as historical analogs for this magnitude of single-day decline often lead to a 3-6 month consolidation period. For Polaris (PII), the stock is approaching a strong historical support level at $45.00, which might attract value-oriented buyers. However, per FactSet, 6 of 14 analysts have lowered their price targets today, suggesting that the recovery will be slow. The third, Polibeli Group (PLBL), which fell 16.5%, remains a high-risk speculative play; with limited institutional coverage, any mean reversion is likely to be ephemeral unless the company releases a clarifying statement regarding its liquidity position. The disconnect is that many retail participants are attempting to “catch the falling knife” in these names, ignoring the fact that liquidity often evaporates in oversold conditions.

Outlook & Risk Assessment

The selloff is poised to deepen tomorrow if the 10-year Treasury yield maintains its position above 4.25%, which would likely trigger further outflows from growth-tilted small caps. The catalyst calendar is thin, but the focus shifts to mid-week regional manufacturing surveys, which could amplify the contagion risk in the industrial sector if they print below the consensus estimate of 48.5. We are monitoring for a “capitulation” volume surge on the major indices as a potential reversal signal, but as of now, the market lacks the buying conviction to reclaim daily moving averages. Bear case: SPX breaks the 5,000 psychological level, which would force further systematic deleveraging from CTAs and risk-parity funds. Bull case: A sudden cooling in the DXY (currently at 98.1) could provide the necessary relief for these battered sectors to stabilize.

Watch: $5,000 on the S&P 500—a breach here triggers a technical stop-loss cascade.

Key level: 4.35% on the 10Y Treasury—if this level is breached, equity multiples will likely face immediate downward adjustment.

Trigger: Any daily close above the 20-day moving average on DOO would be the first signal of a potential institutional entry, but until then, remain sidelined.